When it comes to building tax-free retirement income, two options come up more than any others: the Roth IRA and the Indexed Universal Life (IUL) insurance policy. Both can play a powerful role in your retirement strategy — but they work very differently, and the right choice depends entirely on your goals, risk tolerance, and financial picture.

Before we dive in, check out this excellent breakdown from David McKnight of The Power of Zero:

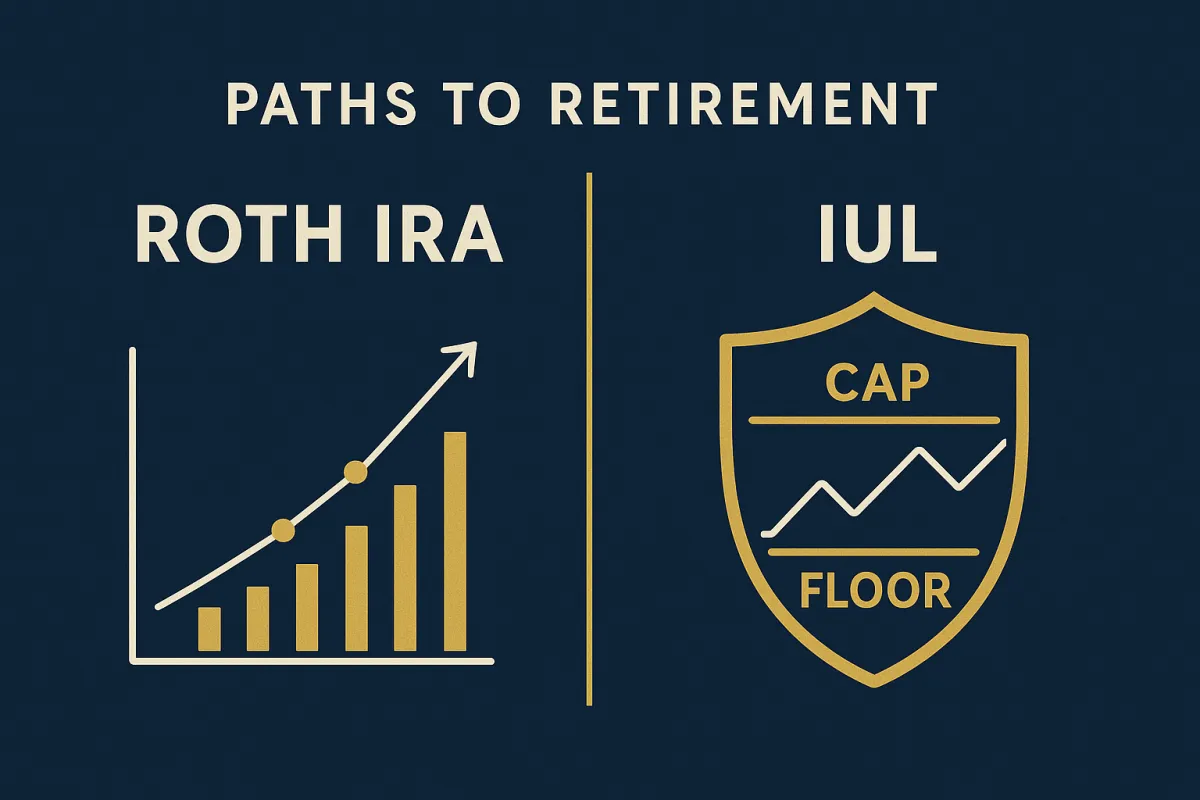

The Core Idea

Both IULs and Roth IRAs can provide tax-free retirement income — but they get there through very different paths. Understanding those differences is the key to making the right decision for your situation.

�� Roth IRA: Simple, Low-Cost, Market-Driven

The Roth IRA is a retirement account designed for long-term investing. You contribute after-tax dollars, your money grows tax-free, and qualified withdrawals in retirement are also tax-free.

- Investment flexibility: Stocks, ETFs, mutual funds, and more

- Low fees: Especially when using index funds or ETFs

- Tax-free growth and withdrawals in retirement

- Contribution limits apply (subject to IRS annual limits and income thresholds)

- Market-linked returns: Higher long-term upside potential, but your balance can fluctuate with market conditions

The Roth IRA is often the go-to recommendation for straightforward, cost-efficient retirement savings — and for good reason.

��️ Indexed Universal Life (IUL): Protection, Flexibility, and Tax-Free Loans

An IUL is a permanent life insurance policy with a cash value component tied to a market index (such as the S&P 500). It's not a direct investment in the market — instead, your cash value grows based on index performance, subject to a cap (maximum gain) and a floor (protection from market losses).

- Downside protection: A floor (often 0%) means you won't lose cash value due to market downturns

- Growth potential: Gains credited based on index performance, up to the cap

- Death benefit: Provides life insurance protection for your loved ones

- Living benefits: Some policies include riders for critical or chronic illness

- Tax-free loans: In retirement, you can borrow against your cash value tax-free

- Higher fees: Especially in the early years — proper structure is critical

The IUL shines when you want the combination of growth potential, downside protection, insurance benefits, and tax-advantaged income in retirement.

⚖️ Side-by-Side Comparison

| Feature | Roth IRA | IUL |

|---|---|---|

| Tax-Free Growth | ✅ Yes | ✅ Yes |

| Tax-Free Withdrawals | ✅ Qualified distributions | ✅ Via policy loans |

| Contribution Limits | Yes (IRS limits) | No |

| Market Downside Risk | Yes | No (floor protection) |

| Death Benefit | No | ✅ Yes |

| Fees | Low | Higher (especially early) |

| Return Potential | Higher (uncapped) | Moderate (capped) |

So, Which One Is Right for You?

There's no universal answer — and honestly, for many people, the best strategy involves both. The right choice depends on your retirement goals, your tax situation, your risk tolerance, and whether the insurance features of an IUL are valuable to you.

What I can tell you is this: making this decision without understanding all the moving parts can cost you — either in missed growth, unnecessary fees, or gaps in protection.

Let's Find Your Best Path Forward

Whether you're leaning toward a Roth IRA, curious about an IUL, or just trying to figure out where to start — I'm here to help you cut through the noise and find a strategy that actually fits your life.

Reach out or send me a message and let's have a no-pressure conversation about your retirement picture.

Your future deserves a strategy built around you — not a one-size-fits-all answer.